Current market situation

The historical corn purchases from China, reduced planted corn acreage in the U.S. and poor weather conditions in Brazil have continued to fuel low corn stocks-to-use ratio in the U.S. This has raised the December 2021 pre-planting corn price of $4.52 per bushel (bu) to $5.33 per bu. Comparing this with the five previous December corn contracts shows that prices are about 70 cents per bu higher. Ultimately, higher corn prices create higher feed costs for feedlots. Kansas State’s Focus on Feedlot report shows that for steers the cost of feed is approximately $105 per hundredweight (cwt) this year, compared to $80 in 2020 and the $79 per cwt between 2015-19. Placing heavier cattle that require less corn while on feed is one way to control costs while continuing to supply market-ready live cattle to meet consumer demand.

Domestic meat demand has created incentives to continue to place cattle even with concerns over packing plant capacity. Over the last two years, domestic meat demand has been strong, and consumers have continually shown that they were willing to spend money on beef even at high retail prices. Some of this is likely due to government transfers and income saved by not eating at food service over the last 18 months. However, since quarantine restrictions have eased from the pandemic, consumers continue to buy large quantities of beef at retail. Ultimately, demand for retail and food service beef is passed down from consumers to feedlots via the live cattle price. Current CME live cattle (LC) prices suggest there is a lot of forward carry in the market – October 2021 LC was trading at $122 while the April 2021 LC was trading at $136. There continue to be incentives to place cattle even at higher corn prices.

Cattle on Feed report

Each month, the USDA releases the Cattle on Feed report. This report surveys feedlots with 1,000-plus capacity (85% of all fed cattle) and provides an estimate of the number of cattle being fed for slaughter. The report includes data on inventory, placements, marketings and other disappearance. The September USDA National Agricultural Statistics Service (NASS) Cattle on Feed report had Sept. 1 feedlot inventories at 11.234 million head, 98.6% of last year. August marketings were 1.885 million head, 99.6% of one year ago, and August placements were 2.104 million head, 102.3% of one year earlier. August placements and marketings were both slightly higher than average pre-report estimates but within the range of analyst forecasts.

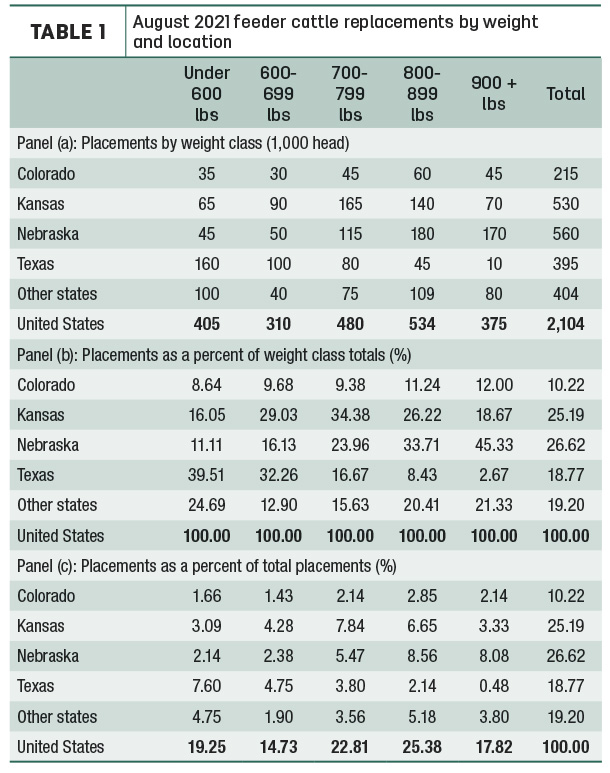

Increase in heavy placements

So how did feedlots take the current supply and demand conditions and translate them into placement decisions by weight class? For states with large amounts of fed cattle (Colorado, Kansas, Nebraska, Texas), the report breaks down the number of feeder cattle placed on feed by weight class. The August placements were the largest placement total for that month since 2011. Placements in the 900- to 999-pound category were up 19.6% over August 2020 (see panel (a), Table 1). About 43% of placements weighed more than 800 pounds, continuing the general trend of heavier placements. Nebraska continues to place heavier cattle relative to lighter cattle. This is distinctly different than Texas, which favors lighter feeder cattle. Kansas is more moderated, primarily placing middleweight cattle. It shows the market preference and specialization in the feeder to fed cattle market (See panel (b), Table 1). Overall, the large increase in heavier placed cattle in August will frontload future production depending upon ending harvest weights and average daily gain performance. Slower average daily gain or higher ending harvest waits would push total beef production further into 2022. Further, more of this product will likely be of Choice- or Prime-quality grade product. While there's been a lot of talk about feedlot currentness and whether they have been able to work through capacity issues, current placement patterns suggest that there continues to remain substantial optimism for higher live cattle prices among feedlots.

Part of a larger trend

These placement patterns highlight a larger trend that has been underway for some time in the different markets. Nebraska has continually started to place heavier cattle in the market relative to Texas for the last 10 years. Feeder cattle weighing 800 pounds plus have steadily increased, while cattle weighing less than 800 pounds have all decreased. For example, placements of feeder cattle weighing between 600-699 pounds decreased from 100,000 head per month in 2000 to 75,000 head per month in 2019. Similar broad decreasing trends are observed in feeder cattle less than 600 pounds and 700-799 pounds The months that heavier feeder cattle are placed likewise reveal how feedlots are managing the inflow of feeder cattle.

Summary

The most recent Cattle on Feed report revealed that most additional placements were heavier cattle. This is in line with the current market situation of higher feed prices yet continued strong domestic demand for beef products. Nebraska was the largest placer of heavier cattle in this month. However, this is part of a larger trend within Nebraska that has moved away from feeding middleweight feeder cattle (600-800 pounds) and more toward heavier cattle (800 pounds plus). These placement patterns will likely result in more beef production in early 2022 that is of Choice or better. ![]()

This article was originally published by the University of Nebraska – Lincoln Center for Agricultural Profitability.

-

Elliott Dennis

- Assistant Professor

- Livestock Marketing Economist

- University of Nebraska – Lincoln

- Email Elliott Dennis