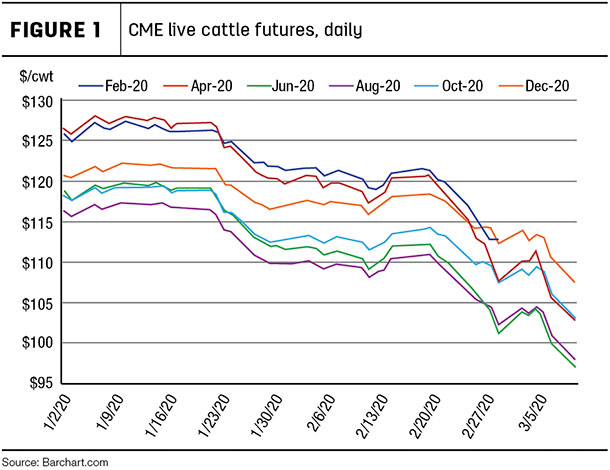

Why did April 2020 live cattle futures lose $10.675 per hundredweight (cwt) from Friday, Feb. 21 to Friday, Feb. 28? Why did it recover $3.70 per cwt over the next three trading days?

Why did it then skid $5.525 per cwt by week’s end (see Figure 1)?

Your crystal ball guess may be as good as mine. I may be being a bit facetious here. A market analyst’s job is to be able to tally this all up. Right?

However, how COVID-19, formerly known as the 2019 novel coronavirus or 2019-nCoV, will play out and how long it will take to come under control are unquantifiable. The cattle market fears the disease will spread and slow the global economy, which will trim beef demand. No one can predict the what/when/where of the next outbreak and its impact on cattle prices. Many wonder if the Monday, March 9 contract low of $102.85 per cwt for April 2020 live cattle futures was a major bottom. We cannot know that because of the unknown future impacts of COVID-19 among all the other factors impacting the market.

The fed cattle market is not alone

Feeder cattle, lean hogs, corn and soybeans are all down. Albeit at different levels and across different timeframes. All have incredible volatility, too. Our 24/7 news cycle makes sure markets have something to react to. Futures markets anticipate the worst or best. And in doing so, they sometimes overreact.

Stock market jitters and concern over national and global issues have recently dominated cattle markets. But staying in tune with the fundamentals is equally important. Supply and demand are the cornerstones to evaluate any market. Equilibrium among those two factors will find a price, even when a lot of noise exists around the price, as is currently the case.

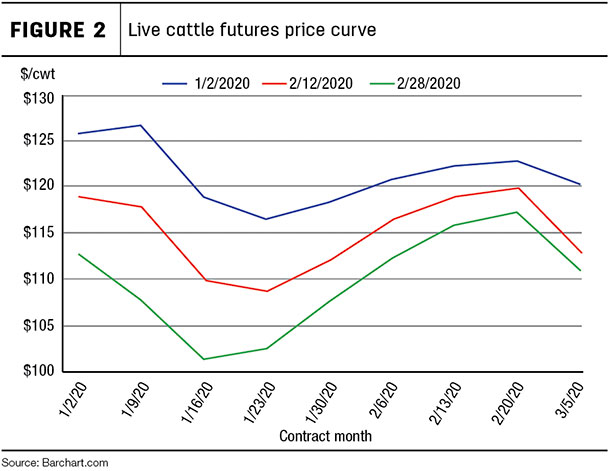

Consider the price curve

The futures price curve provides one “guess” on where future prices may go. It plots the prices of futures contract months on a curve going out in time. Now, technically, this isn’t a bet on where future prices will be; it’s today’s price for a commodity to be delivered in the future and a tool for buyers and sellers to manage (share) price risk.

Intuitively, most people might assume you would pay less today for something that will be delivered many months or a year-plus from now, given the time value of money, that the receiver of the money could earn interest and the whole “bird in the hand” argument where a producer is likely to book guaranteed future revenue for a discount. That sort of a price curve, where the further-out futures contracts are priced lower, is called backwardation. The terms negative carry and premium market are synonymous with backwardation. Many commodities markets are frequently in backwardation, especially when the seasonal aspect is taken into consideration.

But price curves don’t always work that way. Many times, a further-out contract is priced higher in a curve structure. That’s referred to as contango. The terms positive carry and normal market are synonymous with contango. Why would traders pay more today for a commodity they won’t get in months or over a year? Buyers may think supply will be tighter in the future. The opposite would be true for a market in backwardation, where supply is expected to be greater in the future.

The same rationale follows for demand. If short-term demand is stronger than is expected in the long term, with all else equal, chances are the market structure will tend toward backwardation. But if demand is expected to get stronger, the market may be in contango.

Where is the market now?

The live cattle futures market recently switched from backwardation to contango. We will attempt to explain some of the fundamentals behind the switch.

Live cattle entered a bear market after it made highs in early January 2020. The bear gained momentum due to large beef supplies compared to a year ago. January 2020 beef production, at 2.39 billion pounds, was 3% above 2019 according to USDA’s Livestock Slaughter report. Cattle slaughter totaled 2.9 million head, up 2%. The average live weight was up 12 pounds from January 2019, at 1,375 pounds. The rise in beef production has come at a time when supplies of other proteins are also quite large. January 2020 pork production was up 8% from January 2019, with broiler production up 6%.

The increase in supply has resulted in lower prices, although the price decline has seemingly been larger than would be expected, especially since most of this supply increase had already been priced into the market. Based on calculations from the Livestock Marketing Information Center, the retail all fresh beef demand index for 2019 was 109, which is the fourth-highest level in the past 20 years and 2% stronger than 2018. Beef demand has been strong.

But futures markets trade expectations of future demand, not necessarily what’s happening today. The spread of COVID-19 threatens domestic and especially export demand. Lockdowns, various degrees of restrictions on mobility, closures of food service and markets are all occurring in some capacity worldwide.

Beef consumption should rebound when the COVID-19 fears ease. However, what are already high prices could temper demand, and consumers may shift to lower-priced proteins in a slowing economy. Again, futures markets are forward-looking, and they trade daily based on the information available and how it is interpreted.

Market fears current fundamentals

On Jan. 2, 2020, the one-year backwardation – nearby month futures contract (Feb. 20) versus the one-year deferred contract (Feb. 21) – was $3.575 per cwt or 3% (see Figure 2).

On Feb. 28, 2020, the one-year contango was $2.925 per cwt or 3%. The same pattern holds true for the April 20 to April 21 price curve. The current contango in live cattle points to a combination of ample supplies and lower demand – be it feared, perceived or actual lower demand. Contango and backwardation is a real-time indicator of supply and demand fundamentals.

If you were bullish live cattle when February and April 2020 futures contracts were trading over $125 per cwt in late December and January, some critics would have said you cannot be bullish on live cattle because we were in backwardation, and the far-out futures were signaling lower prices. If you believed the backwardation, you would have been bearish when you should have been bullish.

The same is true for recent times. So maybe the change to contango is a significant sign that perhaps little downside is left, at least in the front end of the market. It also could be signaling that current demand for live cattle is much weaker than expected.

Contango and backwardation

Most simply, contango is when deferred futures prices are anticipated to be higher than the nearby prices. Backwardation is when deferred futures prices are anticipated to be lower than nearby prices.

Understanding contango and backwardation can assist in analyzing the current supply and demand characteristics of any commodity market. Many factors go into the collective market wisdom that sets these curves on a day-to-day basis, but the key is: They are dynamic and a key component of futures markets.