The headline numbers were: placements down 1.8 percent, marketings down 0.6 percent and Jan. 1 cattle on feed up 1.7 percent. The year-over-year increase in cattle on feed continues to get smaller. Another month of reduced placements, the fourth in a row below the year before, means that total placements in 2018 were 1 percent below 2017. So fewer cattle were placed from a larger cow herd and larger calf crop.

One of the more interesting numbers in the report was the quarterly estimate of the breakdown of steers and heifers on feed. Heifers on feed totaled 4.41 million head, up 6.2 percent from the year before. That was the most Jan. 1 heifers on feed since 2012. Slightly fewer steers (0.8 percent) were reported on feed compared to a year ago. Slaughter data, through early February, indicated heifer slaughter is up 8.5 percent, while steer slaughter is down about 0.6 percent.

The delayed February Cattle on Feed report will be released on March 8. Several confounding factors will affect that report, including bad weather in feeding country and rising fed cattle prices.

Cattle inventory this week

The cattle inventory report will be released Thursday, Feb. 28. I expect it will show a small increase in beef cow numbers. We are likely about to the end of the growth part of the cattle cycle, as heifers on feed in the Cattle on Feed report and cow and heifer slaughter data indicate. There are several other numbers in the report worth looking at beyond the headline all-cattle-and-calves number.

Watch for the number of heifers held back for replacement. That should show another decline as the cycle peaks out. Also watch for the calf crop estimate, in particular for revisions to past years’ data based on placement patterns. The number of cattle on small grains pasture will be interesting, also gauging supplies of feeder cattle to come from wheat pasture country.

The markets

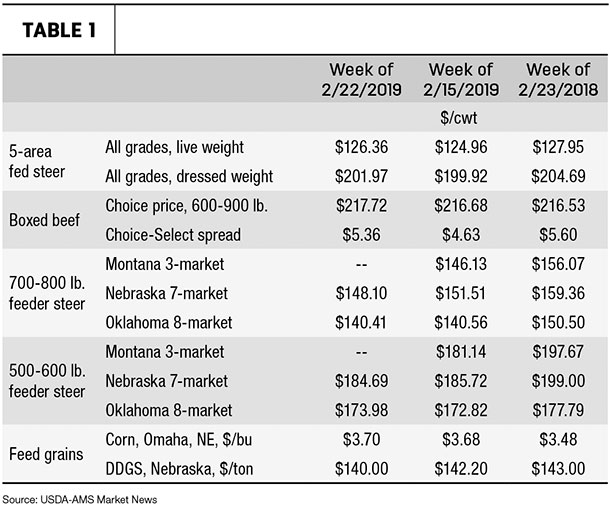

The Choice beef cutout continues to run ahead of last year, with the Choice-Select spread about the same as a year ago. Calf prices across all weights in the Southern Plains continue to be below a year ago. But lighter weight calves have tended to increase in price over the last couple of weeks, while heavy feeders have declined. Cull cow prices in the same area have given up most of their early February $8 per cwt gain. ![]()

David P. Anderson is a Texas A&M AgriLife Extension economist. This originally appeared in the Feb. 25, 2019, Livestock Marketing Information Center In The Cattle Markets newsletter.