At the same time, the corn crop continues in good-to-excellent condition, and estimates for both per-acre yields and total production continue to increase as the summer progresses.

As a result, corn prices continue to decline. The declining corn prices have been a positive factor in the continuing increases in feeder cattle prices.

Click here or on the image above to view it at full size in a new window. (PDF, 2.2MB)

The USDA National Agricultural Statistics Service (NASS) released its five-year revisions of inventory estimates for the major livestock species recently. In its five-year revisions, NASS raised a number of cattle inventory estimates back through Jan. 1, 2008.

Despite the changes, the revisions changed very little and have little or no effect on current or future inventory dynamics.

Monthly average dressed weights of all cattle slaughtered have continued their seasonal increase into September. Historically, dressed weights typically peak during October and decline into the next year, often reaching seasonal lows in April-May.

However, in 2011, 2012 and 2013, peaks were later than is typical, with a November peak in 2013 and not peaking until the following year in both 2011 (peaking in February 2012) and 2012 (peaking in January 2013).

In 2014, federally inspected dressed weights bottomed in May at 790 pounds per carcass, 8 pounds above the May 2013 low and a record high for a May average.

Further, declining corn and soybean meal prices have encouraged producers to keep cattle on feed longer, which could also contribute to heavier average dressed weights over the near term.

Cheaper feed and favorable pasture conditions – combined with reduced placements of heifers on feed (which produce smaller, lighter carcasses), fewer cows (which also produce smaller carcasses) in the slaughter mix, and an increase in the relative proportion of larger, heavier steers in the slaughter mix – will likely lead to significantly heavier average dressed weights for the remainder of 2014 and into 2015.

However, any increases in dressed weights likely will not completely offset the decline in slaughter numbers, which is expected to lead to continued year-over-year declines in total beef production.

Increasing cattle and beef prices will also motivate cattle feeders to try to pull feeder cattle forward – that is, to try to place younger, lighter feeder cattle on feed – in order to meet likely increased demand for fed cattle.

Generally, lighter weight placements yield lighter fed cattle and, to the extent this tendency holds, pulling cattle forward will tend to result in more but potentially lighter carcasses.

The impact on beef production will be ambiguous because more lighter cattle placed into and marketed from feedlots may or may not result in greater beef production.

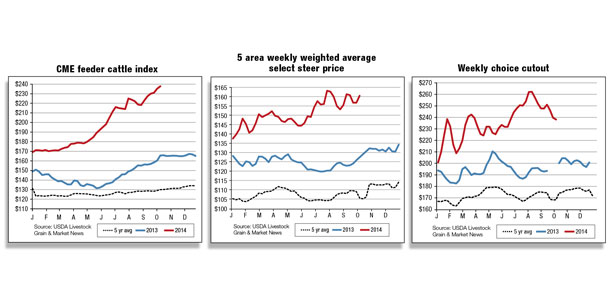

At the same time, when prices follow a typical seasonal pattern, they peak in the spring, then drop in summer and fall, with lows often occurring in late summer. In 2012 and 2013, prices bottomed earlier in the summer, then began generally rising until the following spring peaks.

This year, fed cattle prices appear to have reached lows in late spring/early summer and continue to move erratically higher, jumping almost $6 per hundredweight (cwt) in one recent week.

With weekly cutout values 6 (choice) to 8 (select) percent off their early August peaks, increases in cutout values are not keeping pace with increases in fed cattle prices, and beef packers’ margins are being squeezed again.

Packers will likely try to reduce kills in the weeks ahead in an attempt at raising cutout values to stay ahead of fed-cattle price increases. If successful, this action would ease some of the pain associated with buying $160-plus per-cwt fed cattle and slow the narrowing of packer profit margins.

Both average monthly choice retail and all-fresh beef prices reached new record highs in July. However, the higher prices reportedly make featuring beef to draw retail customers more difficult and less likely.

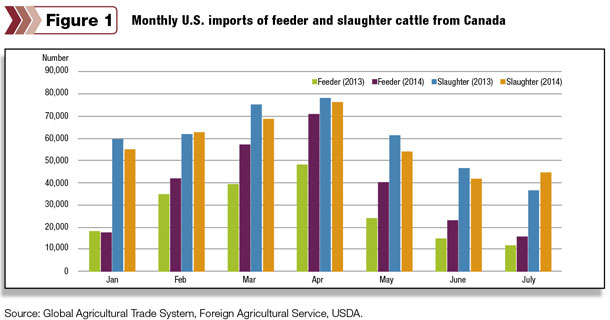

Strong demand for feeders support cattle imports

U.S. cattle imports totaled 1.297 million through July 2014, an increase of 12 percent from last year. Imports have increased most from Canada (up 11 percent) due to strong demand for feeder cattle.

Canadian feeder cattle shipments through July are 39 percent higher than last year, while imports of slaughter animals have declined 4 percent (see figure 1).

Thus far in 2014, imports of feeder cattle account for 29 percent, and slaughter animals account for 59 percent of total cattle imports from Canada. Imports are also up from Mexico (up 12 percent). Despite lower cattle supplies in Mexico and talk of rebuilding, strong U.S. prices continue to draw cattle across the border.

The forecast for U.S. cattle imports in 2014 is 2.150 million, up 6 percent from 2013. Imports are forecast at 2.175 million in 2015. While strong U.S. demand will continue, reduced inventories in both Canada and Mexico are expected to limit stronger growth in shipments.

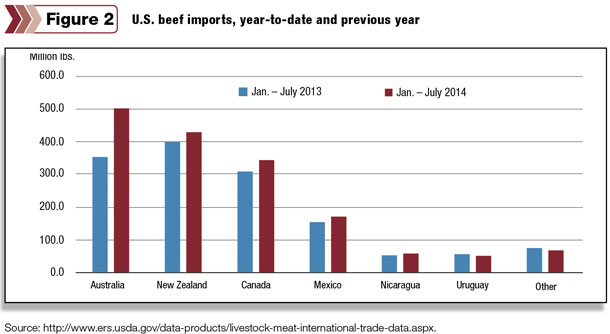

U.S. beef imports strengthen, exports slow in July

U.S. beef imports surged during July, bringing this year’s cumulative total through July to 1.627 billion pounds, 15 percent higher than a year earlier.

Imports from Australia totaled 97.0 million pounds during July, 71 percent higher than July 2013 and the highest single-month total from Australia since April 2009. Imports have also increased notably this year from New Zealand (up 8 percent), Canada (up 11 percent) and Mexico (up 11 percent) (see figure 2).

Demand for imported processing beef has been strong this year due to declining U.S. beef production. Through Aug. 30, 2014, federally inspected cow and bull slaughter is down 13 percent from a year earlier, leading to lower domestic supplies of lean beef. Imports were up only 1 percent during the first quarter but have increased steadily since March.

Higher imports have been facilitated by higher production this year in Australia.

Drought has persisted in Australia’s cattle-producing regions, leading to an 11 percent increase in cattle slaughter through July. Beef production has increased 9 percent, offset somewhat by lower-weight animals. Pasture conditions have improved in New Zealand this year, leading to a reduction in cattle slaughter.

However, New Zealand beef exports are up 6 percent year-to-date, with the U.S. accounting for just over half of exports. The forecast for U.S. beef imports in 2014 was raised to 2.684 billion pounds, an increase of 100 million pounds. The forecast for 2015 was also raised to 2.7 billion pounds.

Strong import demand is expected to continue throughout the forecast period due to lower U.S. beef supplies and strong U.S. beef prices expected to draw supplies from abroad.

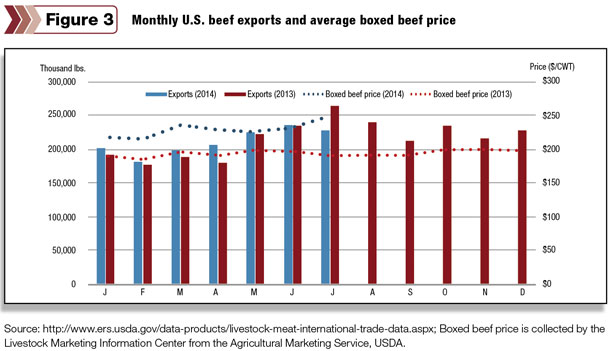

After increasing in each of the first six months of 2014, U.S. beef exports cooled during July. Exports fell 13 percent from the previous year’s level, largely due to lower shipments to Canada (down 26 percent) and Hong Kong (down 32 percent).

July’s downturn in exports indicates that higher U.S. beef prices are beginning to impact trade (see figure). The average price of boxed beef was almost 30 percent higher in July 2014 than a year earlier. Exports to Canada in particular have fallen this year (down 22 percent), further impacted by a weaker Canadian dollar.

Despite considerably higher prices, U.S. exports through July are still marginally above last year’s level. Demand has been robust from Asia, including higher cumulative-year exports to Hong Kong (up 36 percent), South Korea (up 22 percent) and Taiwan (up 9 percent).

Shipments are also up 24 percent to Mexico, making it the second-largest market for U.S. beef.

Japan remains the top market, although shipments have been lower than a year ago. Japanese imports of beef from all countries are down almost 9 percent this year, but the U.S. has increased its market share at the expense of imports from Australia.

The forecast for U.S. beef exports in 2014 is 2.620 billion pounds, 1 percent higher than 2013. Exports are expected to decline in 2015 to 2.525 billion pounds as high prices are expected to weaken export demand.

Kenneth Mathews is an analyst for the USDA-Economic Research Service. USDA-ERS analysts Sahar Angadjivand and Lindsay Kuberka contributed to this report.