This year’s calf crop is estimated at 36.3 million head, which is 3.5 percent larger than in 2016 and 6.5 percent larger than in 2015. The January 1, 2017, cattle and calves inventory was up 5 percent from January 1, 2015. The number of beef cows was up almost 7 percent over the same period.

The U.S. cattle herd began the expansion phase of its production cycle during 2014. The herd on July 1 was 6.9 million head, or 7.2 percent larger than on July 1, 2014.

The estimate for commercial beef production in 2017 was revised higher at 26.7 billion pounds, mainly due to relatively large second-quarter cattle placements and the impact on fourth-quarter cattle slaughter.

Based on the relatively large number of cattle available outside feedlots, it is anticipated that a greater number of cattle will be placed on feed in the remainder of 2017 to bolster commercial beef production in 2018. The 2018 forecast is raised to 27.4 billion pounds.

Heifer retention slows, signaling more feeder cattle

Although growth in the cattle herd implies increased availability of heifers for feeding, there are signs that slower heifer retention for addition to the beef herd may affect supplies of cattle for feeding.

Heifers in feedlots with 1,000 head or greater capacity on July 1 were up 10.6 percent from 2016, and thus far this year, heifer slaughter is up nearly 4 percent. Although to some extent this likely reflects the large supply of heifers due to herd expansion, the number of heifers on feed as a percent of total on-feed numbers increased from 33.7 percent in 2016 to 35.6 percent.

Although comparisons to 2016 are not possible, the Cattle report estimated that heifers retained for beef cow replacement were 2 percent below 2015. Replacement heifers represented 14.5 percent of the cow inventory, lower than 2014-2015, but above the percentages of 2007-2012, a period of relatively strong cow liquidation.

A lower percentage of beef replacement heifers would tend to indicate a leveling off in the expansion of the herd in 2018. To the extent that heifer retention has slowed, it will further increase feeder cattle supplies for placement on feed. Based on the NASS Cattle report, 37.7 million head of cattle were estimated to be available outside feedlots on July 1, 2017, which was 1.6 million more head than on the same date in 2015.

Cattle prices to soften in second half of 2017

Based on NASS Cattle on Feed data through June 2017, net placements in feedlots with 1,000 head or greater capacity during the second quarter reached 5.5 million head, a 10.5 percent increase since 2016 and the highest since 2003.

Further, based on the NASS Cattle report, the estimated number of cattle on feed in all size feedlots on July 1, 2017, reached 12.8 million head, 5.8 percent higher than in 2015. This was the highest total number of cattle on feed reported for a month since 2006.

The larger-than-expected number of calves placed in feedlots increases the likelihood of greater steer and heifer marketings late in the third quarter and early in the fourth quarter, providing an abundance of fed cattle from which meatpackers can purchase supplies.

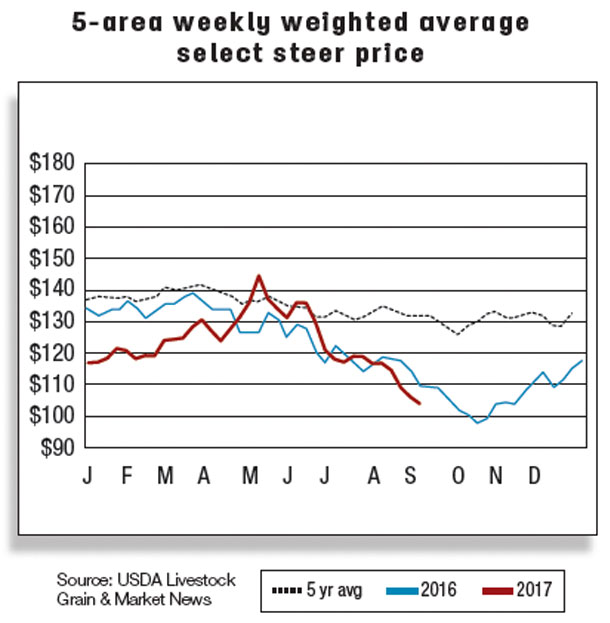

As a result, the third-quarter price for 5-area Choice steers is forecast lower to $113 to $117 per hundredweight (cwt) and to $110 to $116 per cwt in the fourth quarter.

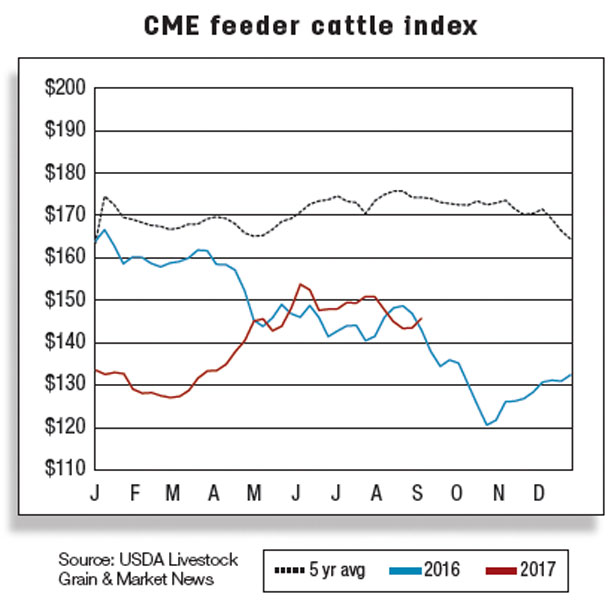

Similarly, with more cattle outside feedlots, and lower fed cattle prices expected to pressure cattle feeders’ returns, the average price for feeder steers weighing 750 to 800 pounds is forecast lower in the third and fourth quarters to $146 to $150 and $141 to $147 per cwt, respectively.

Cattle/beef trade

During the first half of 2017, U.S. beef exports increased by 15 percent while imports declined 7 percent year-over-year. U.S. cattle imports and exports increased in first-half 2017 compared to first-half 2016.

Beef exports up in the first half of 2017

U.S. beef exports during the first half of 2017 increased by 15 percent from a year ago, to 1.3 billion pounds. Beef exports were higher year-over-year in each month during the first half of 2017: January (+21 percent), February (+19 percent), March (+25 percent), April (+15 percent), May (+3 percent) and June (+12 percent).

Major export destinations during this period were Japan, South Korea, Mexico, Canada and Hong Kong, together accounting for approximately 83 percent of total exports. Exports to Japan were up 26 percent from the same period a year ago at 402 million pounds, which represented 30 percent of the total U.S. beef exports in the first half of 2017.

Higher domestic production and lower prices likely enhanced the export competitiveness of U.S. beef during the period.

Higher domestic production and lower prices likely enhanced the export competitiveness of U.S. beef during the period.

Export forecasts for the second-half 2017 and the first-quarter 2018 have been revised downward about 1 percent from the previous month due to prospects of increasing competition from other major beef exporters and to the anticipated impact of the recently announced Japanese safeguard designed to raise the tariff on U.S. beef imports from August 2017 through March 2018. Regarding the imposition of the safeguard, USDA noted, in part:

The government of Japan has announced that rising imports of frozen beef in the first quarter of the Japanese fiscal year (April-June) have triggered a safeguard, resulting in an automatic increase to Japan’s tariff rate under the WTO on imports of frozen beef from the U.S.

The increase, from 38.5 percent to 50 percent, will begin August 1, 2017, and last through March 31, 2018. The tariff would affect only exporters from countries, including the United States, which do not have free trade agreements with Japan currently in force.

Beef exports in 2017 are forecast at 2.8 billion pounds, 9 percent higher than a year earlier. This is due to greater available U.S. beef supplies and to anticipated increased shipments to export destinations outside of the top five major U.S. beef export destinations. For the first half of 2017, 41 million pounds more beef were shipped to destinations outside of the top five export destinations, an increase of 22 percent compared to the same period a year earlier.

Beef imports down in first half of 2017

First-half 2017 U.S. beef imports declined 7 percent from year-earlier levels to 1.5 billion pounds. Notable declines during the first 6 months came from Australia (-34 percent) and New Zealand (-17 percent), likely due to tighter domestic supplies in Oceania. These declines were partially offset by increased imports from Brazil (+42 percent) and Mexico (+31 percent).

U.S. beef imports in third-quarter 2017 are expected to be 710 million pounds, 5.5 percent below a year ago. Fourth-quarter imports are expected to be 610 million pounds, almost 5 percent below a year earlier.

Total 2017 beef imports are forecast at 2.8 billion pounds, a 6 percent decline from 2016. Greater domestic beef supplies and continued herd rebuilding in Oceania will likely limit incentives to import beef.

Live cattle trade increased

The U.S. live cattle trade increased during the first half of 2017. Imports increased by 8,000 head to 958,000 head, while exports increased by 38,000 head to 63,000 head. Declines in cattle imports from Canada during this period were offset by increases from Mexico. Higher feeder cattle prices in the U.S. likely provided incentives for Mexico to supply more feeder cattle during the period. ![]()

Analyst Lekhnath Chalise contributed to this report.

References omitted but are available upon request.

Russell Knight is a market analyst with the USDA – ERS. Email Russel Knight.