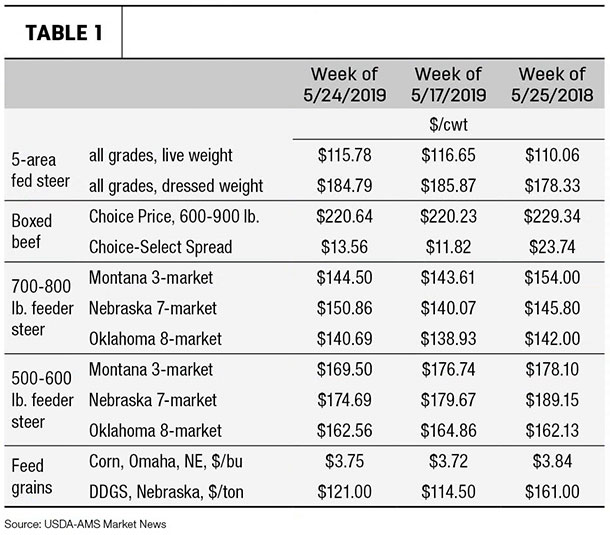

The USDA NASS Cattle on Feed report for May was released last Friday. For as large as the numbers are, it has the potential to be bullish. Placements in feedlots during April totaled 1.84 million head, 9% above 2018. During April, placements of cattle weighing less than 700 pounds were similar to last year and the prior five, while placements of cattle weighing more than 700 pounds were 8% above last year and 11% above the prior five years. These are strong placements, but prior to the report, expectations were for this figure to be 13.5% above the prior year with a range of 8.6% to 18.9% above the prior year. Compared to expectations, these placements are modest.

Cattle on feed for the slaughter market in the U.S. for feedlots with capacity of 1,000 head or more totaled 11.8 million head on May 1, 2019. The inventory was 2% above May 1, 2018. This is the highest May 1 inventory since the series began in 1996. However, this number is 1% below the prior month. Further, cattle on feed over 90 days declined very slightly, and cattle on feed over 120 days are down sharply – over the 200,000 head. Cattle on feed over 120 days start to decline seasonally during May, this was seen, but more sharply than typical. The report also shows on-feed numbers for Iowa, Minnesota, Nebraska and South Dakota clearly lag last year. But placements in all those states except Minnesota were very aggressive during April. Cool wet weather is hampering cattle feeding as well as corn planting, but on-feed volumes are turning the corner.

Marketings of fed cattle during April totaled 1.93 million head, 7% above 2018. These are very strong marketings as well. Expectations were for increases of 6.6% over the prior year with a range of 5.9% to 7.1%, so the actual is at the top end of this range. Feedlots are marketing aggressively and did not place as strongly as expected during April. From the cattlemen's perspective, this is exactly what was needed during the prior month – before animal slaughter weights begin seasonal increases, and beef tonnage availability starts its march higher. We'll see how the futures and cash markets react through the trading week.

The markets

What do the technical say? Live cattle and feeder cattle futures have held steady at support planes following the trend breaks and sharp down-moves after April 23rd. June sits above $109, August and October sit above $106, and December sits above $110. The late summer and fall complex of feeder cattle contracts sit above $142 to $143. Both live and feeder cattle are likely due to a correction following the rapid move at the end of April and the stalling of that move in May. The recent Cattle on Feed report may be the catalyst to start the correction. A 32% to 50% trade is reasonable but after that, I want to assess trade volumes, domestic demand, beef tonnage and likely volumes of completing meat before forming expectations for cattle markets post-June. ![]()

Stephen R. Koontz is a professor in the department of agricultural and resource economics at Colorado State University. This originally appeared in the May 28, 2019, Livestock Marketing Information Center’s In the Cattle Markets newsletter.