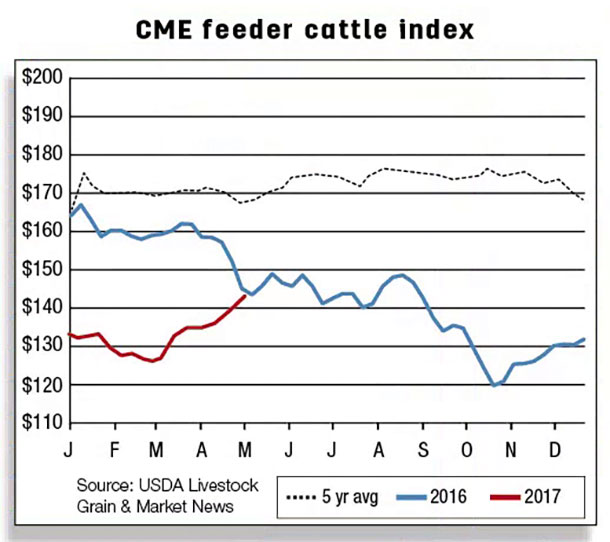

To the extent demand for calves to graze out these areas increases, prices of lighter-weight calves may find support. However, the timing of movement of these calves off pasture and into feedlots will likely impact both the level of placements and the price of heavier-weight calves in the coming months.

Feeder and fed cattle prices were supported by relatively strong demand during the first quarter, but packer demand has likely weakened as margins have been squeezed by weakening wholesale prices.

The timing of beef sales ahead of grilling season may influence packer demand during the quarter, but second-quarter steer and heifer slaughter will likely reflect the marketing of the large number of cattle placed on feed in late 2016.

Weekly dressed weights for cattle during March were slightly higher than previously expected, and second-quarter carcass weights were raised, helping to support an increased forecast of commercial beef production in the first half of 2017.

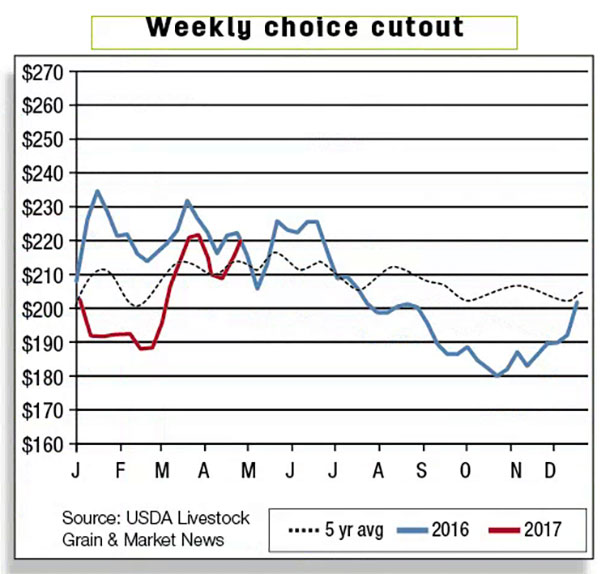

Wholesale beef cutout values strengthened toward the end of the first quarter; however, this is not surprising, given the tendency for both Choice and Select beef cutouts to gain momentum heading into the spring grilling season, when the market transitions from lower-valued end cuts to more expensive middle meat cuts.

The weekly boxed beef cutout data (USDA-AMS report LM_XB459) reports Choice cutout values that advanced from mid-February’s low of $188.93 to $223.12 per hundredweight (cwt) on March 24, with Select cutout values also gaining impressively over the period. However, wholesale beef prices have declined since the last week of March.

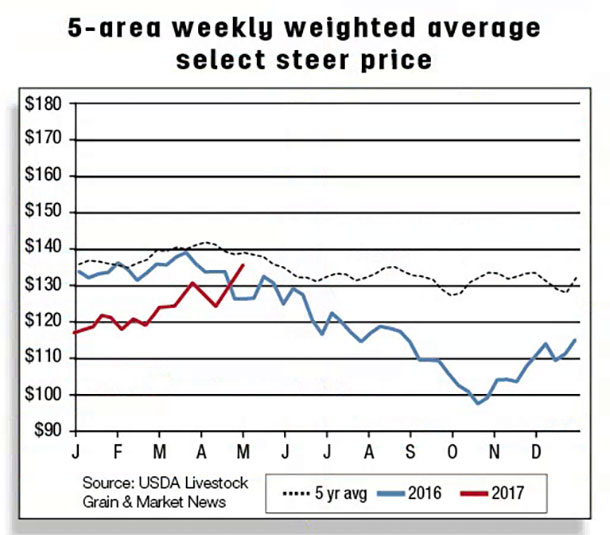

The gains in the boxed beef cutout values through late March are the result of significant gains in beef middle meats (i.e., the rib and loin primals). However, boxed beef cutout values began showing signs of weakness in late March, squeezing packer margins and likely pressuring fed cattle prices. The first-quarter 5-area weighted steer price averaged $122.96 per cwt. The 5-area weekly weighted steer price has weakened from $127.38 during the last week of March to $124.33 per cwt in early April.

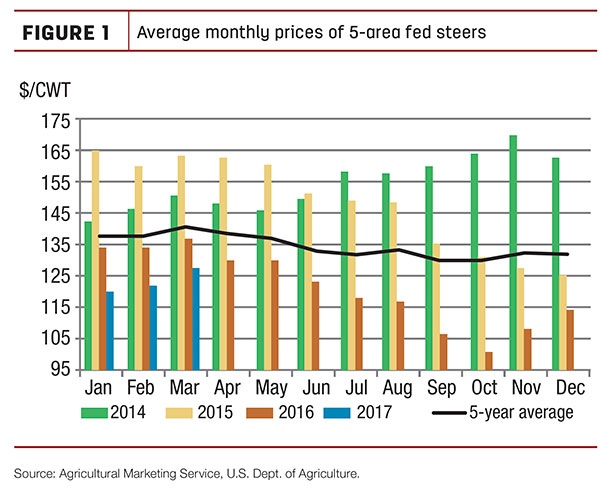

Beef packers appear to be backing off recent higher prices for fed cattle. Fed steer prices reached $132 per cwt in the third week of March before declining to average $124 per cwt in the first week of April. Fed cattle prices in the second quarter are forecast to average $117 to $121 per cwt, pressured by large supplies of cattle available for slaughter from late 2016 and early 2017 feedlot placements.

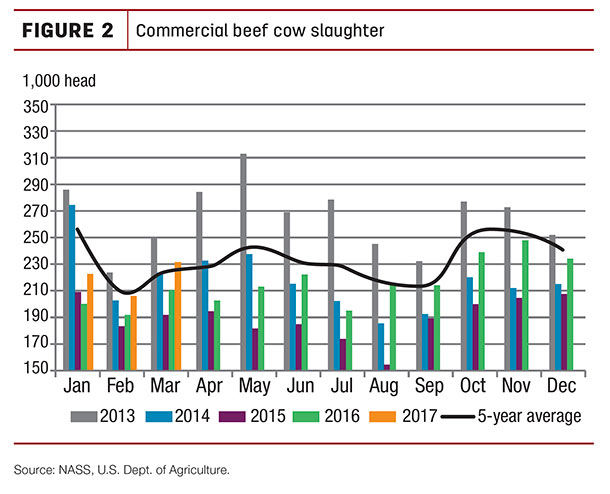

Estimated federally inspected weekly total cow slaughter for the first quarter was up about 5 percent compared to the same period in 2016. Beef cow slaughter is almost 10 percent higher year-over-year. However, cow slaughter as a proportion of the Jan. 1 beef cow herd is only slightly higher than 2016 but below the average for 2012-2016, a period which included drought-induced liquidation.

First-quarter prices for cutter cows were estimated at $62.63 per cwt, and prices for the remaining quarters for 2017 are likely to tick higher. Second-quarter cutter cow prices are forecast to average $63 to $66 per cwt.

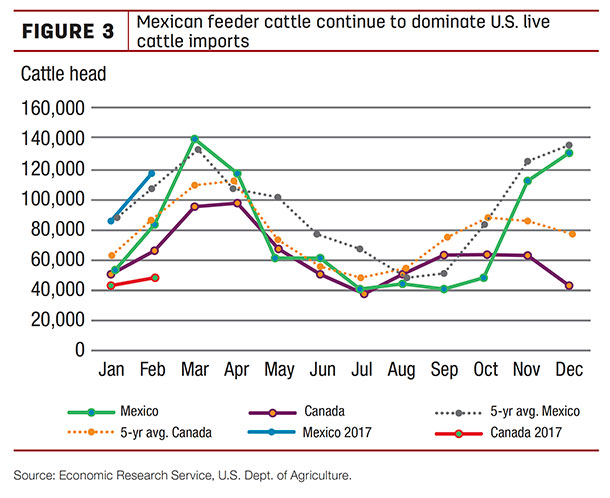

Mexican feeder cattle imports continue to show strength

In February 2017, U.S. live cattle imports increased by 27 percent from the previous month to 168,473 head, up 11 percent from the same period a year ago. More than 85 percent of the feeder cattle imported from Mexico were in the 400- to 700-pound weight range, while almost all of the feeder cattle imported from Canada were over 700 pounds.

For most of 2016, there was not a large difference between the number of cattle imported from Mexico and Canada, but since November 2016, live cattle imports from Mexico have been significantly higher than imports from Canada.

January and February imports from Mexico were above the five-year average, while imports from Canada were below it. The strength of the U.S. dollar relative to the Mexican peso and a rebuilding of the Mexican herd are likely contributing factors to this uptick in imports from Mexico.

In February 2017, U.S. live cattle exports were up 66 percent from a year ago to 8,299 head; however, volume was down 36 percent from January. Mexico and Canada were the primary export destinations, responsible for 80 percent of total U.S. live cattle exports. February U.S. live cattle exports to Mexico declined sharply (69 percent) from the previous month to 1,049 head, 57 percent lower than the same month a year ago.

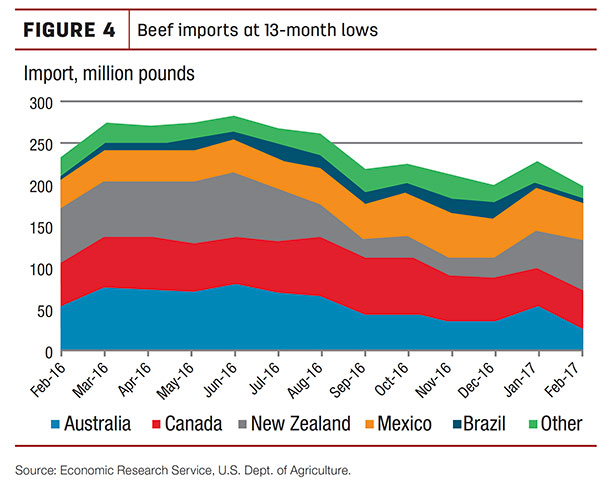

U.S. beef imports expected to decline in first quarter 2017

In February 2017, the U.S. imported 200.5 million pounds of beef, 14 percent below a year ago.

This is likely due to lower supplies in several key importing countries coupled with relatively large supplies of processing-grade beef in the U.S. New Zealand, Canada, Mexico, Australia and Nicaragua were the top five suppliers, accounting for 93 percent of total U.S. beef imports in February 2017. U.S. imports from Australia declined 42 percent from year-earlier levels, likely due to continuing herd rebuilding in Australia.

Imports from Canada also declined by 9 percent to 6 million pounds in February from the previous month, and imports from New Zealand declined by 11 percent to 44.5 million pounds from last year. Some of the declines were offset by 22 percent higher imports from Mexico. First-quarter 2017 U.S. beef imports are estimated at 685 million pounds, a 14 percent year-over-year decline.

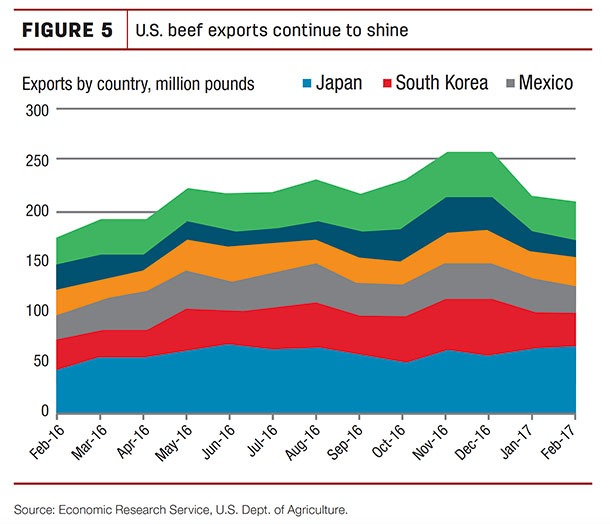

Lower U.S. beef prices bolster year-over-year increase in exports

Increased domestic supplies have dampened U.S. beef prices, which continue to make U.S. beef exports more competitive. In February 2017, U.S. beef exports increased by 19.3 percent from the same period a year ago to 205.5 million pounds.

The U.S. exported about 84 percent of February’s volume to Japan, South Korea, Mexico, Canada and Hong Kong. Each market saw double-digit percentage point increases year-over-year for February except for Hong Kong, which imported 19.2 percent less. ![]()

Analyst Lekhnath Chalise contributed to this report.

Russell Knight is a market analyst with the USDA – ERS. Email Russell Knight.