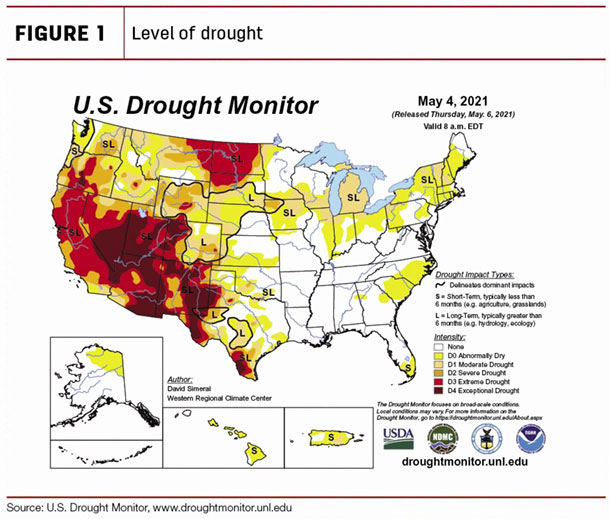

As reported by the U.S. Drought Monitor on May 4, 2021, 66% of the country was experiencing some level of drought, compared to just 31% the same week last year (see Figure 1).

Further, 23% of the nation is in the top two worst categories of extreme to exceptional drought, whereas last year less than 1% fell under these designations. This has put 36% of the cattle inventory in an area experiencing drought, and 14% of the herd is in the worst two tiers.

Furthermore, based on the USDA National Agricultural Statistics Service (NASS) Crop Progress report for the week ending May 9, 2021, 44% of pastures are in poor to very poor condition compared to just 16% for the same week last year.

These effects on pastures have likely led to greater hay usage and, consequently, to higher hay prices. According to the latest USDA NASS Crop Production report, hay stocks on farms on May 1, 2021, were lower by 12% from last year. Although stocks are 21% above May 1, 2019, levels, they are below the five-year and 10-year averages for the same period.

Based on elevated drought levels, poor pasture conditions and higher hay and feed costs than a year ago, it is expected that the pace of placements in feedlots in 2021 will be faster than was expected last month, which may result in lower year-over-year placements in 2022. Further, if pastures do not develop as the year progresses, the pace of slaughter for breeding stock is likely to increase in 2021, lowering expectations for the beef cow inventory on Jan. 1, 2022.

Pace of slaughter constraining beef supplies

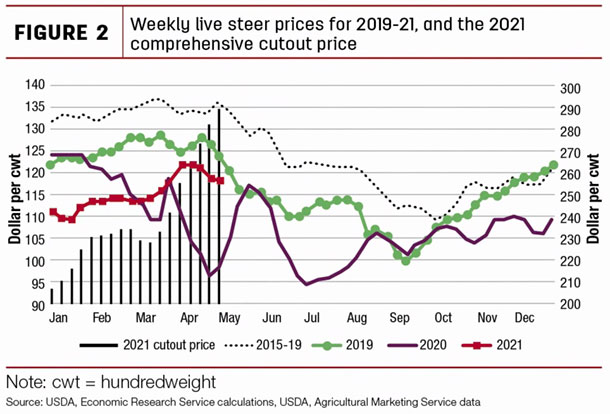

In first-quarter 2021, the beef industry was faced with greater volumes of market-ready fed cattle compared to recent years, a result of greater year-over-year placements in second-half 2020 and a packing industry struggling to process cattle in a timely manner. Consequently, maximum weekday volumes of federally inspected fed cattle slaughter were 2,000 to 3,000 below pre-pandemic levels. However, the average weekday slaughter volume in first-quarter 2021 was about 5,000 head below last year and over 1,000 head below 2019, which suggests fed cattle slaughter was about 25,000 head fewer per week.

However, packers largely made up for the limitation through increased Saturday slaughter levels that average about 21,000 head more than 2020 and about 30,000 head more than in 2019. As a result, on April 1, 2021, feedlots had 11% more cattle on feed over 150 days than last year and about 1% more than in 2019.

Packers appear unable to increase weekday slaughter levels to process the market-ready supply in a timely manner as the sector enters a period of typically higher fed cattle slaughter. This appears to be in part due to labor disruptions that packers have dealt with since the beginning of the pandemic – but also interruptions in slaughter due to extreme weather in February and scheduled plant maintenance events. Because this time period spans the peak of the pandemic’s impact on packing plants, it is necessary to make comparisons to 2019 statistics to appreciate the changes. In the first six weeks of second-quarter 2021, average weekday slaughter levels have fallen to about 3,000 to 4,000 head below 2019, and Saturday kills are just 5,000 head above 2019. As a result, thus far in second-quarter 2021, packers are processing about 10,000 to 15,000 head fewer a week than in 2019.

2021 production raised; 2022 production to drop first time in seven years

The 2021 beef production forecast was raised to 27.9 billion pounds, a difference of 260 million pounds from the previous month. Second-quarter 2021 beef production was raised slightly on higher non-fed cattle slaughter that more than offset anticipated lower fed cattle slaughter due to concerns with packer capacity. Carcass weights were also adjusted higher as weights have stayed relatively flat in a range of 5 pounds for eight weeks in a row, even as they should typically begin to fall this time of year.

Second-half 2021 production was raised on higher anticipated fed and non-fed cattle slaughter. A greater-than-expected number of feeder cattle were placed in first-quarter 2021, raising the expected pace of fed cattle marketed for slaughter. In second-quarter 2021, poor pasture conditions and higher feed costs will likely favor a faster pace of cattle entering feedlots, supporting higher fed cattle marketings in the second half of 2021. Further, in the face of expected tightening forage supplies, producers will likely increase culling of breeding stock – both cows and bulls – in second-half 2021. The USDA AMS report on federally inspected cattle slaughter by region through the week ending April 24 shows recent elevated cow slaughter levels in the Southwest, Southern Plains and Midwest.

Conversely, beef production in 2022 is expected to decline by 2% year-over-year to 27.3 billion pounds, the first drop in beef production in seven years. This is a result of the quickening pace of fed and non-fed cattle slaughter leaving fewer supplies of cattle available for slaughter in 2022. However, carcass weights are expected to increase year-over-year as non-fed cattle will be a smaller portion of the slaughter mix.

Conversely, beef production in 2022 is expected to decline by 2% year-over-year to 27.3 billion pounds, the first drop in beef production in seven years. This is a result of the quickening pace of fed and non-fed cattle slaughter leaving fewer supplies of cattle available for slaughter in 2022. However, carcass weights are expected to increase year-over-year as non-fed cattle will be a smaller portion of the slaughter mix.

Fewer supplies and robust beef demand in 2022 support higher prices

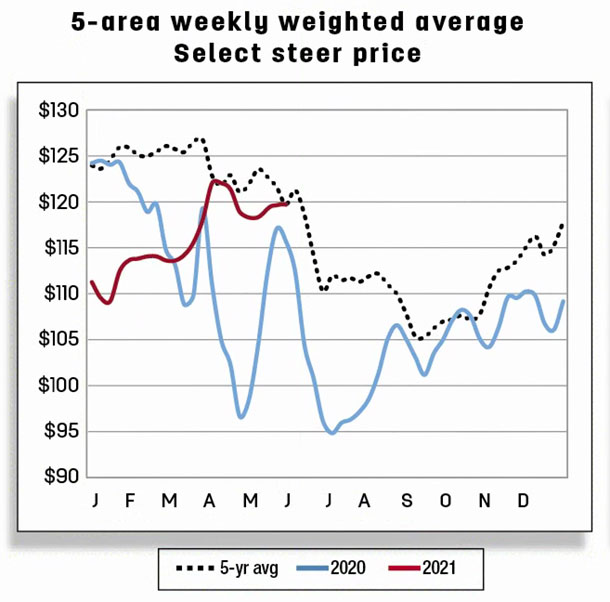

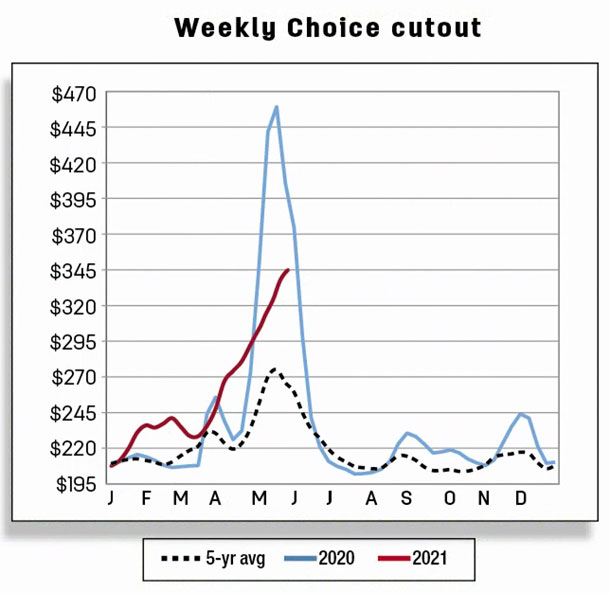

Weekly fed steer prices rallied in April, topping at about $122 per hundredweight (cwt) (see Figure 2), likely in response to the surge in wholesale prices.

Wholesale prices have continued to soar into early May, albeit still below 2020 levels, but fed steer prices have not responded similarly, likely due to the constraint on beef packing capacity.

The second-quarter 2021 fed steer price forecast was raised $1 on current price data, but third-quarter 2021 was lower by $1 because of a greater expected market-ready supply of fed steers at that time. The 2021 fed steer price is forecast at $116.30 per cwt.

The 2022 outlook for the fed steer price is $122 per cwt, a 5% increase year-over-year and the highest price since 2017. Fewer fed cattle marketings and continued robust beef demand are expected to bolster prices in 2022.

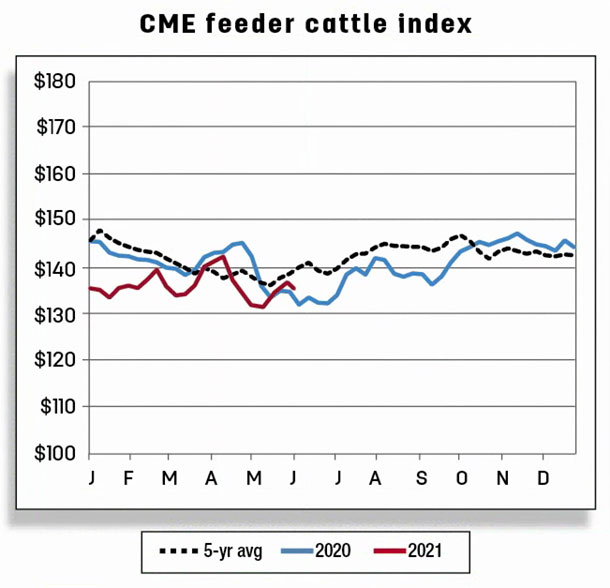

Regarding 2021 feeder steer prices, feedlots are constrained in their ability to market cattle in a timely manner; as producers face poor pasture conditions and rising feed costs, they will compete for space in feedlots in an environment with higher expected feed prices and little optimism for fed cattle prices. Accordingly, the second-quarter 2021 feeder steer price forecast was lowered $1 on current prices, and the third-quarter 2021 price was dropped $2, for a 2021 annual forecast of $139.30 per cwt.

In 2022, if forage production reflects normal growing conditions, higher fed cattle prices and fewer cattle supplies outside feedlots should support improved feeder steer prices year-over-year, but higher feed costs are expected to partially offset that support. As a result, the 2022 feeder steer price is forecast to improve 3% above 2020 to $144 per cwt.

Cattle imports and exports

The U.S. import cattle forecast is lowered by 25,000 head to 1.95 million head in 2021, largely based on current data on imports from Mexico. The annual forecast for 2022 imports is 2.025 million head due to tighter expected cattle supplies in the U.S. The forecast for exports of cattle is raised by 20,000 head to 380,000 head on larger shipments to Mexico and Canada in 2021. The annual forecast for 2022 cattle exports is 350,000 head.

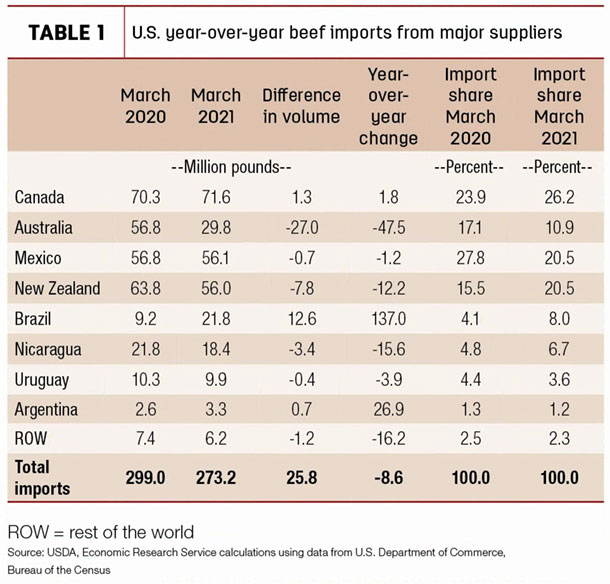

Beef imports up in March but down in 2021 first quarter and remain relatively flat in 2022

Beef imports in March totaled 273 million pounds, down 8.6% (25.8 million pounds) compared to a year ago (Table 1).

This

This

decrease was fueled by low shipments from Oceania (Australia and New Zealand). For Australia, beef exports continue to be limited as inventories have been drawn down by drought the prior year and more heifers and cows are being held back for breeding. Imports from Australia have been down year-over-year since October 2020.

In March, imports from Australia were the second-lowest volume of beef to the U.S. since it started herd rebuilding in 2020. Shipments from New Zealand were also lower in March relative to a year earlier, for several reasons. First, tighter supplies – a result of cattle being kept on pasture longer after favorable rainfalls – has reduced exports. Other competing markets also have pulled beef supplies away from the U.S. in March.

New Zealand’s beef production has remained relatively steady, and its beef shipments to China, Australia and Switzerland have increased by 45%, 15% and 16%, respectively, year-to-date, while New Zealand exports to the U.S. have fallen 7%. Imports from Mexico were down year-over-year, but the total volume shipped was sizable, including Mexico’s second-largest import ever in March.

In contrast, shipments from Brazil registered as the largest volume year-over-year in March since 2007. Canada, which is the top U.S. beef supplier, accounting for more than 26% of U.S. beef imports in March, had a modest increase in March.

Beef imports in the first quarter of 2021 totaled 696 million pounds, down 78 million pounds or 10% from a year ago. In 2020, first-quarter imports were the third-largest in volume since 2006, while annual beef imports were the second-largest on record. Imports from Australia were down 87.3 million pounds in the first quarter and accounted for only 11.7% of the U.S. total beef imports in the first three months, compared to 21.8% in 2020. Despite the increases in percentage share shown for six of the eight major U.S. beef suppliers in first-quarter 2021, the sum of their exports was not large enough to offset the reduction in imports from Australia.

The forecast for beef imports in the second and third quarters was raised by 30 and 10 million pounds from the previous month’s forecast to 790 and 780 million pounds, respectively. This anticipated increase is expected to be driven mostly by North and South America. While the fourth-quarter forecast was unchanged from the previous month, the annual forecast for 2021 beef imports was raised to 2.961 billion pounds.

In 2022, the forecast for the first quarter is relatively flat at 700 million pounds. The annual forecast for 2022 is also relatively flat at 2.95 billion pounds from last year on depressed cattle slaughter and limited exportable supplies in Oceania.

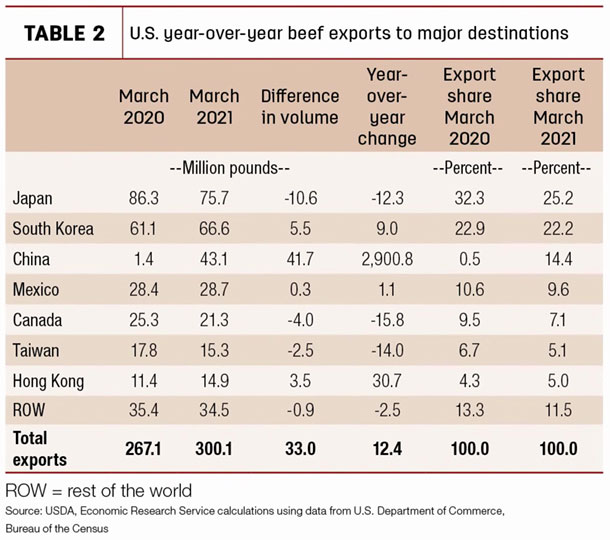

Beef exports up in March on robust shipments to China, but forecast in 2022 is flat relative to 2021

In March, the U.S. exported the most beef (in volume) ever recorded, totaling 300 million pounds, an increase of 12.3% (or 32.9 million pounds) from a year ago (Table 2).

Besides the year-over-year increase in beef shipments to South Korea, Hong Kong and Mexico, there was a significant rise in exports to China. U.S. beef exports there totaled 43.1 million pounds, by far the largest volume the U.S. has ever exported to China.

Year-to-date, China ranks the third-largest U.S. beef destination, surpassing both Mexico and Canada. The rise in exports to China reflects, in part, China’s growing demand for beef and its ongoing challenges with the African swine fever as the country works to rebuild its swine inventory and industry. In contrast, beef exports to Japan, the U.S.’s largest market, were down more than 10 million pounds or 12% from last year.

In March, Japan accounted for 25% of the U.S. total exports, notably lower than the 32% in March 2020. There were some reductions in shipments to other major U.S. beef destinations. Shipments of U.S. beef to Canada, which accounted for 7.1% of U.S. beef exports in March 2021, fell 4 million pounds year-over-year. U.S. exports to Taiwan dropped 2.5 million pounds lower than a year ago to 15.2 million pounds, the lowest for March since 2017.

First-quarter beef exports totaled 797 million pounds, 3.6% larger than last year. Japan and South Korea continue to account for the greatest share of U.S. beef exports. Among major U.S. beef destinations, China’s share increased from less than 1% in March 2020 to over 11% in March 2021. South Korea had the second-largest increase in share of 2 percentage points more than a year ago. The export shares to other major U.S. beef destinations and the rest of the world were all lower in 2021 relative to a year earlier.

The forecast for the second and third quarters was increased by 20 and 15 million pounds from the previous month to 810 and 825 million pounds on expectations for continued strong exports to China. No changes were made to the fourth-quarter export forecast from the previous month. The annual forecast for 2021 beef exports is 3.227 billion pounds. The first-quarter 2022 is forecast to be slightly lower than 2021 due to lower expected cattle slaughter and tighter beef supplies. The 2022 annual forecast for beef exports is 3.225 billion pounds, flat relative to 2021 due to limited exportable supplies.

Analyst Christopher Davis assisted with this report.