Based on USDA Agricultural Marketing Service (AMS) data for actual and estimated federally inspected slaughter of steers and heifers in September, on a daily basis the pace appears to have risen above year-ago levels for a second consecutive month at about 0.5% above last year, while non-fed slaughter is trailing almost 4% below last year. Because of this quicker-than-expected pace of slaughter, the number of fed cattle expected to be slaughtered in third-quarter 2020 was raised, as was cow slaughter.

The pace of fed cattle slaughter was carried over into fourth-quarter 2020, and more cows are expected to be slaughtered. These factors raised the 2020 beef production forecast by 90 million pounds from the previous month to 27.1 billion pounds.

The forecast for 2021 beef production was raised by 10 million pounds from the previous month to 27.4 billion pounds on a slightly more rapid pace of cattle marketings.

Beef demand and packer margins support higher cattle prices

Based on the September USDA National Agricultural Statistics Service (NASS) Cattle on Feed report, there were 9.8% more net placements in August than in the previous year. Combined with the number of cattle in feedlots that were yet to be slaughtered in July because of reduced slaughter capacity in the second quarter, the increased placements pushed cattle on feed on Sept. 1 to above year-ago levels and to the largest number for September since the series began in 1996.

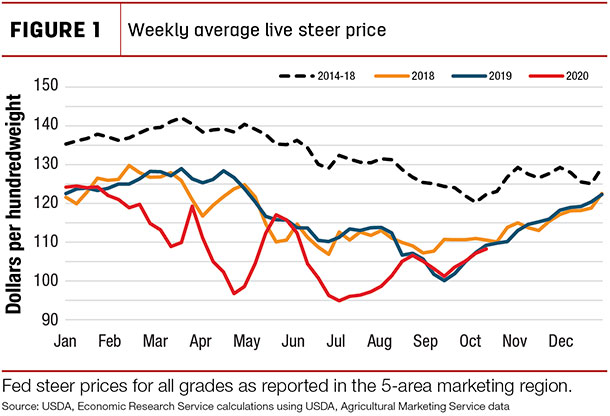

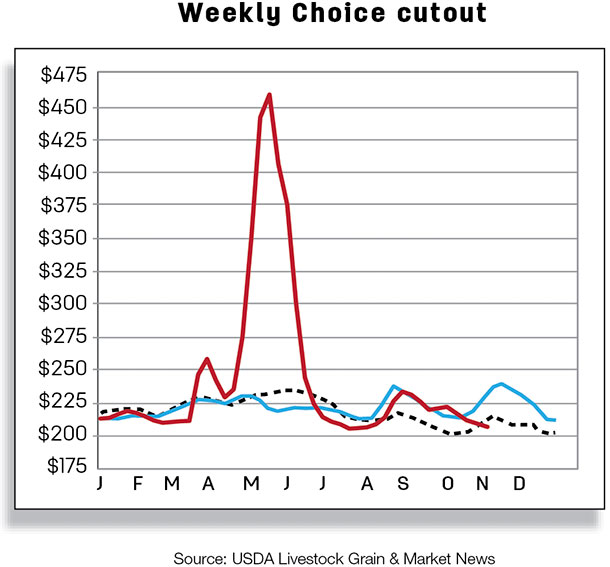

Despite the rising number of cattle on feed, front-end supplies – the number of cattle on feed over 150 days – diminished for the third consecutive month. This is the result of an improving pace of fed cattle slaughter, which was faster than a year ago for the last two months at the time of this writing and above the five-year average. The improving pace, combined with an ample supply of fed cattle at heavier weights, has led to higher expected beef production in third-quarter 2020 relative to 2019. Nonetheless, firm demand and higher-than-year-ago wholesale prices are likely supporting packer margins, as the recent uptick in steer prices remains in line with year-ago prices (Figure 1).

The price forecast for fourth-quarter 2020 was raised by $5 to $109 per hundredweight (cwt) on recent price strength. This strength was carried over into the first half of next year. First- and second-quarter 2021 were raised by $6 and $3 to $113 and $110 per cwt, respectively. This increased the 2021 annual price forecast to $114 per cwt.

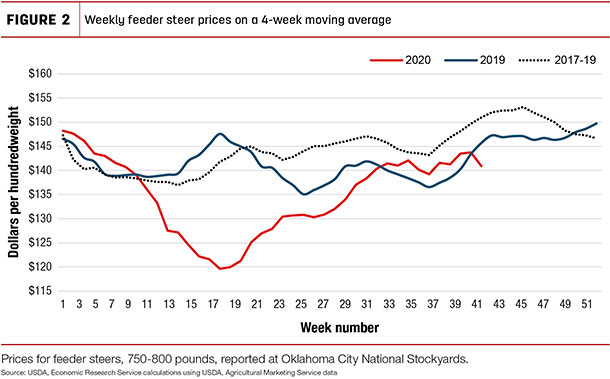

The fourth-quarter 2020 feeder steer price was raised by $3 to $143 per cwt on recent price data for the first week of October and expected seasonal price movement in the fourth quarter (Figure 2).

The adjustment for fed cattle prices in 2021 was carried over into 2021 prices, as the annual price for 2021 was raised by $2 to $139 per cwt.

Beef imports continue robust pace in August

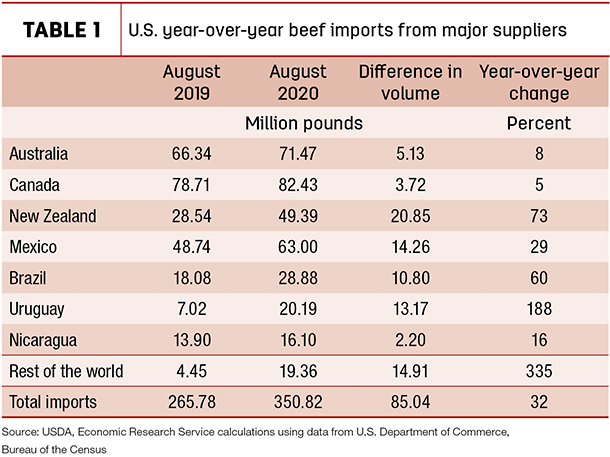

U.S. beef imports in August 2020 were 351 million pounds, up 32% from year-earlier levels (Table 1).

Large import volumes reflect strong shipments from major suppliers, as well as robust growth in shipments from Central and South America.

The major U.S. beef suppliers, Australia, Canada, New Zealand and Mexico, accounted for 76% of August’s total beef imports. New Zealand’s August shipments were the largest for the month since 2003. Beef imports from Mexico in each of the last four months (May, June, July and August) have set monthly records.

Imports of Brazilian beef in August were the largest since December 2008. July 2020 imports from Brazil were also large, just 648,000 pounds less than August’s imports. U.S. beef imports from Uruguay were the largest since September 2007. Beef supplies from Central American countries also continue to rise. As discussed in the previous month’s Livestock, Dairy and Poultry Outlook, Central and South American beef supplies to the U.S. have increased substantially year-to-date.

The forecasts for 2020 third and fourth quarters are raised to 1,025 million pounds (+100 million from the previous month) and 800 million pounds (+75 million) on continued strong demand for processing-grade beef. Imports are expected to remain large. Beef imports for 2020 are 3.447 billion pounds. The annual forecast for 2021 is raised for all quarters to 3.135 billion pounds.

Beef exports above year-ago levels in August

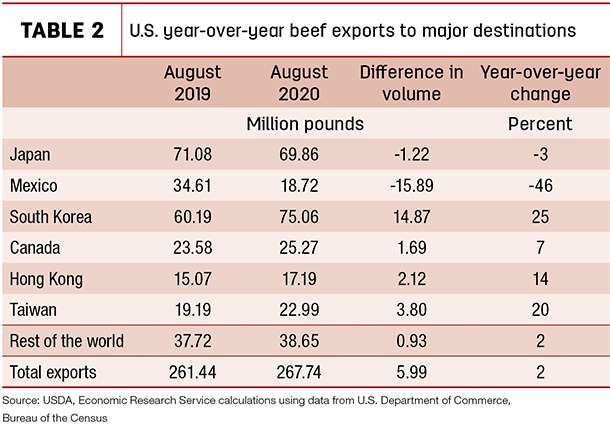

Since March 2020, U.S. beef exports have been higher than year-ago levels. In August, beef exports increased 2%, or 6 million pounds from last year, to 268 million pounds (Table 2).

The U.S. exported 75 million pounds of beef to South Korea, the largest volume on record to that country. Beef shipments to Taiwan in August were the largest to that country (23 million pounds), volume-wise, on record. Beef exports to China have increased over the last several months due to continued demand and the Phase I Agreement. U.S. beef exports to China in August increased 299% year-over-year to almost 11 million pounds. This shipment to China was the largest on record. Other major markets such as Canada and Hong Kong also increased their beef shipments from the U.S.

However, beef exports to Mexico continue to suffer with year-over-year volumes in August almost 16 million pounds less than a year earlier. The reduction reflects the economic downturn in Mexico and the weakness of the peso relative to the dollar. Shipments to Japan, historically the U.S.’s largest beef market, were also lower in August compared to a year ago. Although the reduction in beef shipments to Mexico in August were sizable, increased shipments to South Korea, China and other markets were enough to offset the Mexican and the other reductions year-over-year.

The forecasts for the third and fourth quarters are unchanged from a month ago at the time of this writing. However, in 2021, the export forecasts for all quarters are lowered on a revised global outlook for 2021. The annual beef export forecast for 2020 was unchanged at 2.896 billion pounds, and the 2021 forecast was lowered to 3.08 billion pounds on anticipated lower global demand. ![]()

Analyst Christopher Davis assisted with this report.

Russell Knight is a market analyst with the USDA – ERS. Email Russell Knight.