While the rains are beneficial and are greening pastures, they are not yet enough to alleviate drought impacts on subsoil moisture.

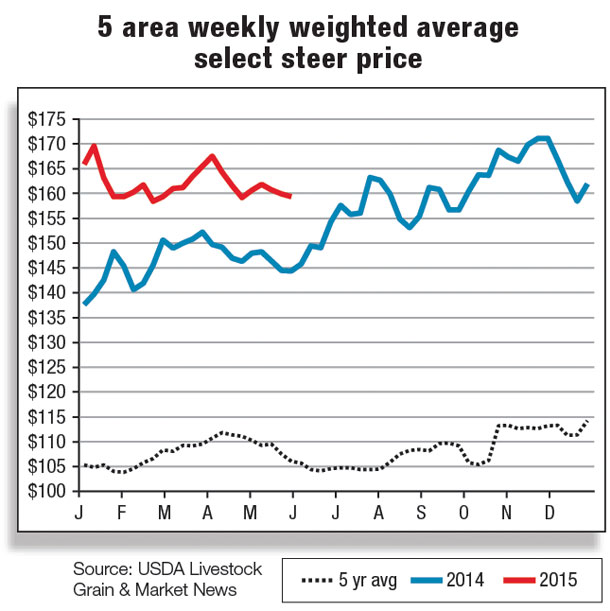

First-quarter commercial cow slaughter was 6 percent below year-earlier slaughter, reflecting the low inventories and the desire to hang on to cows that have or will have calves in 2015.

While commercial beef cow slaughter has been lower year-over-year and declining seasonally, dairy cow slaughter, although still above 2014, has also been declining seasonally.

The combination of fewer cows and heifers in the slaughter mix will result in a higher proportion of steers, which will contribute to heavier average dressed weights of all cattle.

Veal production continues to decline at an accelerated pace due to the high value calves have as feeder cattle instead of as veal. March 2015 commercial veal production was 6.9 million pounds, 21 percent below March 2014’s 8.7 million pounds.

Feeder cattle that were retained to graze out wheat pasture have moved off wheat and to market, some at impressive weights. Average monthly estimated placement weights in March 2015 were the heaviest March weights since 2003 and reflect the improved pasture and forage conditions.

According to the April 2015 Cattle on Feed report, U.S. feedlots with 1,000-plus capacity totaled 10.8 million head on April 1, 2015, up slightly from April 2014. Cattle on Feed listed April 1 steers on feed at 5 percent above steers on feed in April 2014.

There were approximately 10 percent fewer heifers in feedlots on April 1 than in April 2014 – indicating continued interest in heifer retention to support herd expansion.

On a year-over-year basis, average placement weights have been higher since August 2014. With more steers than heifers entering the feedlot, it is expected that weights will continue to increase.

Placements were up in March 2015 compared with March 2014, with cattle of 800-plus pounds, the largest category. At the same time, marketings of fed cattle in March 2015 were the lowest March marketings since the series began in 1996.

The proportionally large numbers of heavy cattle being sold at auction may have implications for steer and heifer slaughter later this summer and fall. This scenario is complicated by the possibility that the current constrained steer and heifer slaughter could persist for the rest of the year.

Heavy slaughter weights – which would also likely consist of steers rather than heifers – would mitigate to some degree the impact of reduced slaughter on total beef production.

Currently, weekly year-to-date federally inspected (FI) slaughter is running a little more than 7 percent below year-earlier slaughter, but beef production is only 5 percent below year-earlier levels; average weekly dressed weights of all FI cattle in April 2015 were nearly 3 percent (almost 23 pounds per carcass) above April 2014’s weight. Further, weights have not yet shown their typical seasonal decline to a May low before again increasing.

Wholesale beef prices decline due to moderate supply pressure

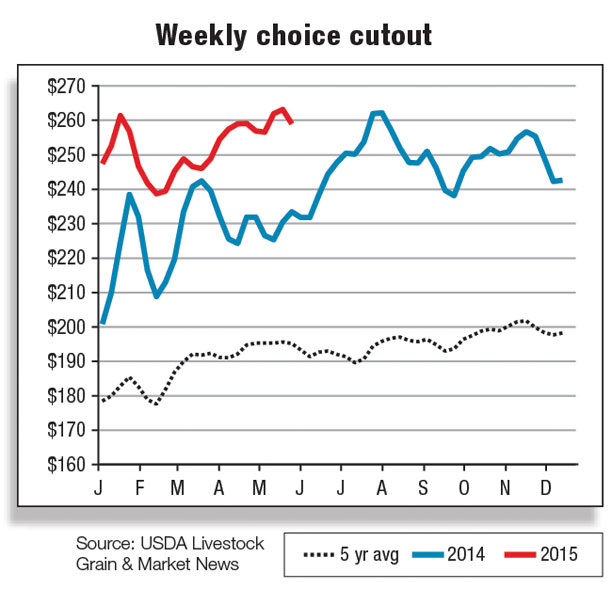

The upward trajectory in wholesale beef prices is beginning to slow as we transition into the spring quarter. The choice cutout has declined a little more than $3 per hundredweight after topping $259 per hundredweight in late April.

At this juncture, it appears domestic demand has weakened modestly in the near term (although remaining strong by historical standards).

For the week ending May 8, 2015, the choice cutout value was priced 13 percent higher than the previous year and 24 percent above the three-year average.

It is also important to consider the supply-side implications of current market dynamics. On a year-over-year basis, weekly cattle slaughter remains lower than 2014; however, in the short term, weekly kills have expanded from unusually tight levels in late March and early April.

Packer margins have improved, providing an incentive to slaughter more animals even though live cattle prices remain relatively high. Increasing weekly kill numbers – in conjunction with historically heavy dressed weights – have led to the decline in wholesale beef prices.

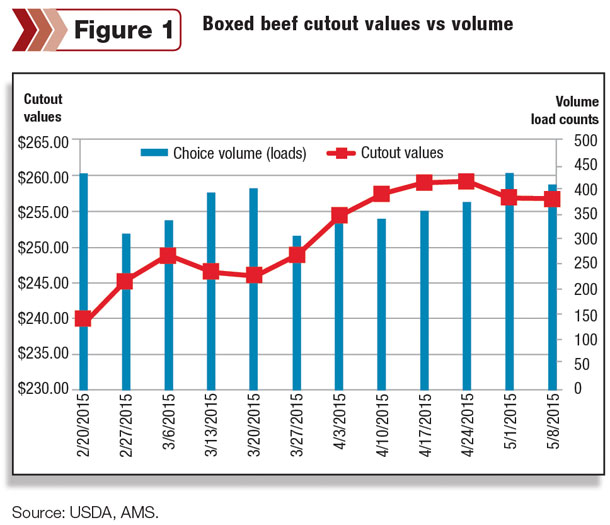

On the other hand, in the midst of tumbling prices, AMS marketing data reports that weekly load counts have been increasing since early March (see figure 1).

Beef imports skyrocket in March, exports remain sluggish

The USDA reported March beef and veal imports at 325.1 million pounds, up 71 million pounds relative to the previous month (February 2015) and 33.3 percent larger than the previous year.

Imports from Australia, New Zealand, Mexico and Canada remain robust. Australia continues to be plagued by severe drought conditions that have led to ongoing liquidation through the first quarter of 2015.

The relative strength of the U.S. dollar, in conjunction with strong demand for processing-grade beef, has helped boost total beef imports this year. First-quarter beef imports totaled 876 million pounds, up 47 percent above first-quarter 2014.

The USDA has raised total beef imports from 2.91 billion pounds to 3.116 billion pounds for calendar year 2015.

Exports, on the other hand, continue to languish as high domestic beef prices and the strength of the dollar remain problematic for U.S. beef exports. March exports were reported at 185.3 million pounds, moderately higher (+7.3 million pounds) than the previous month but 7 percent smaller than March 2014.

While the stronger dollar and high beef prices continue to negatively impact beef exports to Mexico and Hong Kong, March beef shipments to Japan (+9 percent) and Canada (+12 percent) showed signs of moderate improvement relative to last year.

In the aggregate, the USDA is forecasting 2015 exports to reach 2.461 billion pounds, down 4 percent from 2014.

Live cattle imports were reported at a little more than 234,000 head in March, about steady with the previous year but 20 percent higher than in February. Live imports from Canada were reported more than 112,000 head, while shipments from Mexico surpassed 120,000 head.

Noticeable declines in slaughter cattle and cow imports continue to impact overall live imports, but firm feeder cattle demand outweighed those declines in March. Live imports are off to a slow start.

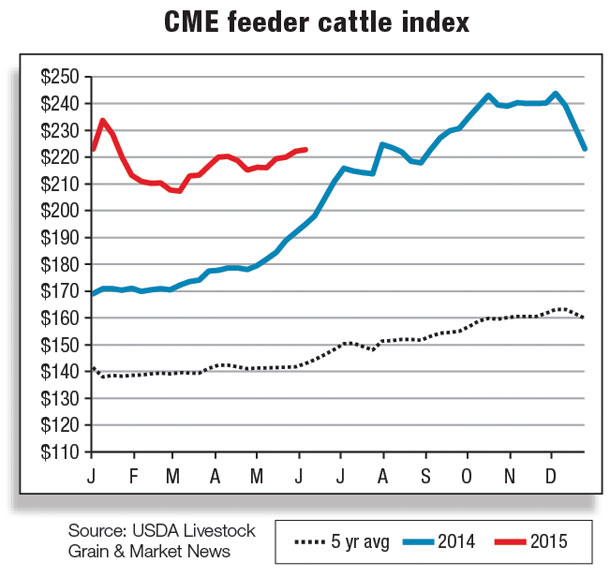

However, demand for live imports is expected to strengthen throughout the remainder of the calendar year as domestic cattle prices are expected to remain high, with cattle inventories constrained and cattlemen holding back heifers to rebuild the domestic cow herd. ![]()

Kenneth Mathews is coordinating analyst for the USDA Economic Research Service. Analyst Mildred M. Haley assisted with this report.

Kenneth MathewsKenneth Mathews

Market Analyst

USDA – ERS