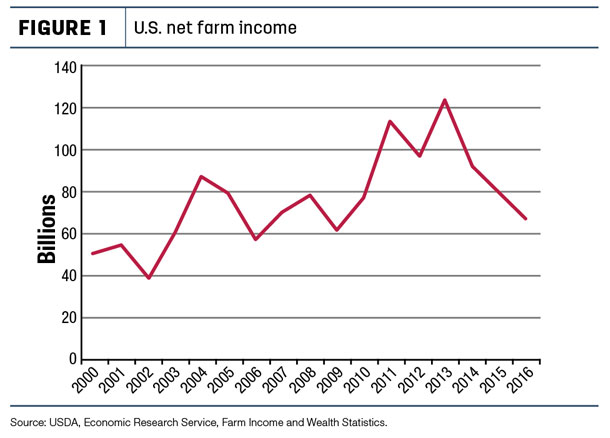

Figure 1 depicts net farm income and net cash farm income for the U.S. since 2000. The range in net farm income is from a low of near $40 billion to a high of more than $120 billion.

Many would agree that a business will generally pay less income tax over the long term if taxable income is somewhat consistent in the sense of either staying the same or in a steady trend, hopefully upward. The most difficult to manage is when one’s taxable income for a business resembles the volatility at the national level.

Many would agree that a business will generally pay less income tax over the long term if taxable income is somewhat consistent in the sense of either staying the same or in a steady trend, hopefully upward. The most difficult to manage is when one’s taxable income for a business resembles the volatility at the national level.

An agricultural producer does not always have control of their taxable income, given market and weather variability. The most difficult to manage is during either very strong profit years or very low profit years.

The Internal Revenue Service (IRS) provides the framework in the way of rulings and court cases to help producers know how to interpret the tax laws Congress passes. Having a knowledge of how certain management decisions could affect their income tax obligation is helpful in managing taxable income. The last time major tax legislation was passed in Congress was 1986.

It appears that with the new administration and new Congress, the time may be approaching for a major reform of the current tax laws to happen. There has not been a great amount of public information about what is being contemplated. Therefore, keep informed of what Congress is doing this year as they debate tax reform and what finally becomes law.

Until major tax reform comes, we have the current law to use to manage taxable income. There are several tools available from the IRS. Plus, there are a few things producers can do to be in a position to use the tools.

Financial records

One of the best ways to position the farm for managing taxable income is by keeping the financial books current. The best records are the result of recording transactions fairly soon after they happen. Time has a way of dimming the best memories.

Knowing what the total revenue and total expenses are is very powerful information when managing taxable income. This will be true no matter how Congress reforms tax laws.

As the end of the tax year approaches, it is even more important to stay up-to-date so one can estimate the tax liability. When knowledge of the total revenue and expenses to date is combined with the projections of each for the rest of the year, adjustments can be made in one or the other and sometimes both before the end of the year.

This can be accomplished by either deferring some transactions or speeding up others depending on the needs and flexibility of the operation. It can only be done effectively with the knowledge gleaned from financial records that are current.

A few words of caution may be in order to help with end-of-year activities. Too often, producers think the only way to reduce taxable income is to buy an asset before the end of the year so it can be totally expensed or deducted in the current year. This may or may not be a good business decision. Sometimes unwise business decisions are made in an effort to reduce tax liability.

Seldom is an end-of-year asset purchase a good business decision if the main purpose is to reduce tax liability for the current year. Think through every asset purchase judiciously.

Depreciation

Tax laws currently provide several tools to manage the speed at which the expense of a depreciable asset is deducted. Section 179, additional first-year bonus depreciation and various depreciation methods offer valuable tools. These may disappear if tax reform happens, so they will not be discussed here, although they should be regarded as very helpful in managing taxable income if they survive.

Reduced tax rate

One opportunity many producers miss out on is the ownership period required for certain gain on sales to qualify for the reduced capital gain tax rate rather than the ordinary income tax rate. This reduced rate can be as little as zero for producers in the 10 or 15 percent tax brackets, to as much as a 10 to 20 percent reduction in higher brackets. This is true especially for livestock producers.

Most items to qualify for the reduced rate require an ownership or holding period of a minimum of 12 months. Sometimes maintaining ownership a few days longer can make a difference. Producers who own breeding cattle are required to own them for 24 months before the gain qualifies for the reduced rate.

Being knowledgeable of these varying holding periods and the reduced rates can help manage taxable income.

It is each American’s duty and responsibility to pay their fair share of government. What represents one’s fair share and how it is calculated has been debated since the birth of our nation. We can discuss what government’s role is and how much government it takes to accomplish that role. We all enjoy good roads to travel on and a safe place to live.

They are not free, so each of us strives to pay our fair share but no more. We should do so within the confines of the law, and when tax is owed, pay with pride because tax is only owed when we make a profit. ![]()