For the past five years, I’ve been writing articles for crop farmers on how to manage the unprecedented amount of income flowing through their operations, and now it is the turn for the livestock producer to worry about what to do with all that extra income.

Agriculture has always been an industry with cyclical income trends. Prior to 2003, the average farm income reported in our annual data would typically go up and down each year, having a good year and then a bad year and then a good year again.

Since then, nothing has been typical when looking at farm income trends, and 2014 seems to be another year that no one projected could have been this extreme.

Cattle producers are looking at astonishing prices for their livestock in 2014, which have many concerned about the tax bill to inevitably follow this period of prosperity.

In addition to the high prices, many producers have received disaster payments from the federal government for losses from 2012 and 2013 in 2014. The combination makes reason for concern for cash-basis taxpayers.

Livestock Disaster Program

In looking at the Livestock Disaster Program payments, there are two separate payments you may have received. The first is a forage program that was to supplement the cost associated with feed losses due to the drought in 2012 and 2013.

Since the program is to give producers the income needed to replace feed, this income will need to be reported on Schedule F for individual taxpayers and will be subject to self-employment taxes.

In other words, since your cost to replace the feed was a Schedule F expense, this payment must be classified as the same type. As a cash-basis taxpayer, it also must be included in taxable income in 2014, or the year you received the payment.

At first you may think that the payments could be deferred like crop insurance, but since the payments are for the 2012 and 2013 tax years, they have already been deferred beyond the year of production, so there is no option for further deferral.

The second program available was an Indemnity Program for the death loss seen in 2013 for either extreme heat or excessive snow. This means this program could have provided income for the loss of either feeding livestock or breeding livestock.

If you were paid for the loss of feeding livestock, the income again must be reported on Schedule F – the same place you would have reported the income from the sale of that livestock – and again will be subject to self-employment taxes.

If, on the other hand, you received payments for the death of breeding livestock, I think there is an argument that the income could be reported as ordinary income on Form 4797 (not subject to self-employment taxes), as the sale of breeding livestock would be reported there.

You will need to make sure your paperwork clearly shows the payment for breeding livestock separate from feeding livestock in order to take this approach. Regardless, this income must be reported on your 2014 tax return, or in the year you received the payment.

Prepaying expenses

There are usually two things that come to mind for the agricultural producers I work with when it’s time to look at reducing income. The first is to buy equipment, and the second is to prepay expenses for next year. Buying new equipment is fun, and prepaying expenses is a habit built in those cyclical years of having alternating good and bad years.

For starters, let’s look at prepaying expenses. With alternating years, prepaying in the good years is a great way to even things out with the next bad year. With multi-year stretches of highly profitable years, prepaying can become a snowball of growing problems. Many crop producers will tell you that prepaying expenses will only work for so long.

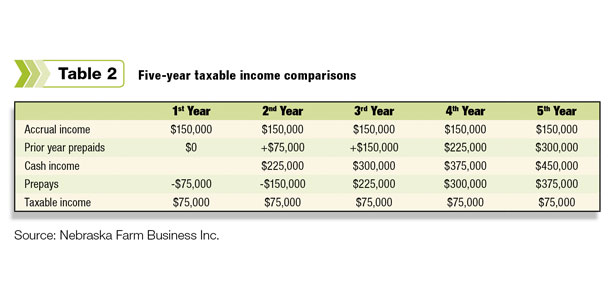

The first year of high profitability, prepayment is easy. The next year, you have to prepay all that and add additional expenses to get to the same place. Let’s look at a quick example (Table 2 ).

If you have on average $150,000 of income and want to keep your taxable income at $75,000, you must prepay $75,000 the first year. That’s usually pretty easy – but the second year, you are short the $75,000 of expenses that you pulled into year one, creating a cash-basis income ($150,000 that you earned again plus the prepaid expenses) of $225,000.

That means in order to get back to $75,000 taxable, you must prepay $150,000. In just five years, you are prepaying $375,000 to stay at your desired income level.

Prepaying expenses is not a bad strategy, but it can’t be the only strategy in periods of long-term profitability.

Capital purchases

Buying capital purchases to reduce taxable income is a longtime favorite strategy by producers and equipment salesmen. The grain producers were given a gift along with their prosperity of enhanced accelerated depreciation.

Their good times came at the same time as a national recession, and one of the federal government’s solutions was to encourage purchasing by the nation’s businesses by increasing the amount of assets they could write off in the first year from $25,000 to $500,000 and adding an additional write-off of 50 percent of any brand-new assets.

These laws have been allowed to expire as of Jan. 1, 2014, and although there has been much talk of another extension, there has been no action taken by Congress to date. While many believe they will take care of this after the elections, it leaves little time for actually purchasing assets prior to the end of the year.

Without congressional action, the law stands that we will have a limit on Section 179 of $25,000 (indexed for inflation) for 2014 and no bonus depreciation. That means that for capital purchases made in 2014, you can fully deduct the first $25,000 you spend – and the remainder will be subject to regular rates.

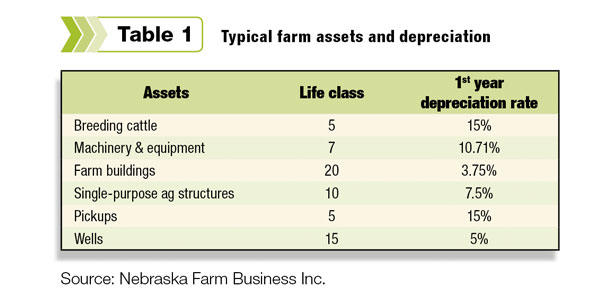

On Table 1 is a chart of some typical farm assets and the first year “normal” depreciation rates.

Without the enhanced accelerated depreciation rates, the immediate benefit of purchasing capital assets is greatly reduced. For example, if you purchase a $100,000 tractor, you could write off the first $25,000, and then the remaining $75,000 would be subject to the rate of 10.71 percent, which would give an additional expense of $8,033, making the total depreciation $33,033.

If that expense reduced self-employment taxes of 15.3 percent and income taxes at a 25 percent rate, the $100,000 purchase would save you $13,312 in taxes the first year.

That means purchasing the asset strictly to save taxes isn’t getting you a very good return on your money. If you needed the $100,000 tractor to improve your operation, the depreciation will be a beneficial part of your plan.

Income averaging

One of the unique tax benefits those in agriculture possess is the ability to use income averaging. This will be a must-use strategy for all livestock producers this year. Income averaging allows cash-basis taxpayers to carry income back to the three prior years and recalculate the tax in those years.

In other words, we get to “pretend” that the income came in those years. It will be especially beneficial since the past three years have been years with lower profitability for livestock producers. This means income that would be pushed into a higher bracket this year could be taxed at the lower brackets you didn’t use.

The income you elect to carry back must be carried back evenly. So if you elect $150,000 of income in 2014, each tax year of 2011, 2012 and 2013 would have $50,000 added to the income reported in those years. This does not affect self-employment taxes. That tax will be calculated on all the income reported in 2014 regardless of any carryback.

Other income-reducing strategies

In many farming and ranching operations, the labor of the family members goes unpaid. In periods of high income, you may consider paying wages. You must pay a reasonable wage for the work done.

For example, you can’t pay a 2-year-old $10,000 per year to help around the farm, but many kids do considerable work around the operation and can be compensated.

This expense reduces your farm income and could be tax-free if their total income is under the standard deduction. This also gives them earned income they could contribute to a Roth IRA. These funds can be used to pay for college expenses but are not looked at for federal financial aid purposes.

Paying your spouse, who also must contribute to the operation, is another option to consider. While this doesn’t create the tax savings that paying your children can, it may mean we can create an employee relationship that you can provide benefits.

The Affordable Care Act has many provisions that limit the flexibility we once had with this strategy, so it’s very important to consult a tax professional about your unique situation before implementing any of these plans.

Retirement plans offer a great way to reduce income today. You can use traditional IRAs that have lower limits or you can consider plans like a SEP plan that allows a significant contribution in high-income years.

Either way, you can use them now to avoid high tax brackets and could convert them to Roth IRAs in years of low taxable income. Either way, putting money into a retirement plan locks the money up until you reach age 59½ (unless an exception applies) or you will face a 10 percent penalty plus tax on the withdrawal.

Contact your tax professional

Remember that paying taxes is not always the evil we often think it is. Paying taxes should mean that you are making money, and that’s a better situation to be in than not making money. It is important that you manage your tax bill responsibility so you are neither creating a nightmare down the road nor paying more taxes than you need to.

The balance of finding ways to have the lowest tax bill over the entire course of your business takes planning and the benefit of a quality tax professional that knows and understands agriculture.

Be sure to consult with your tax professional early this year to have time to make the necessary changes before the end of the year is here.

This originally appeared in the University of Nebraska – Lincoln BeefWatch newsletter